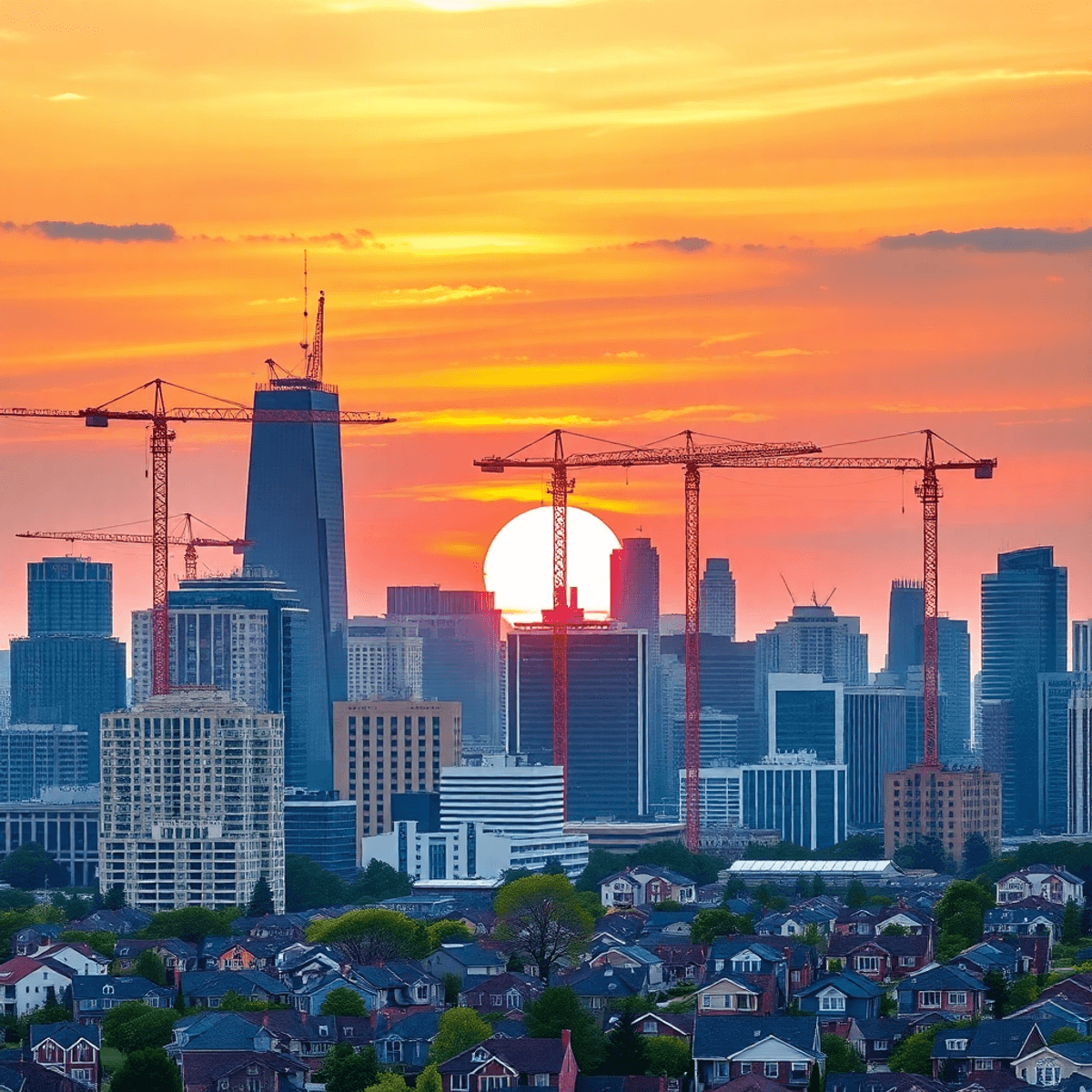

Illinois Housing Market Mid-2025: Soaring Prices Despite Rising Interest Rates

The Illinois Housing Market Mid-2025: Soaring Prices Despite Rising Interest Rates presents a striking paradox. Even as 30-year mortgage rates hover at 6.72%—double the pre-pandemic average—home prices in Illinois, especially within the Chicago metropolitan area, continue to climb. Buyers and sellers alike are navigating a landscape where affordability challenges should, by traditional logic, cool demand. Instead, fierce competition and record-high listing prices define the Illinois housing market in 2025.

Understanding this trend goes beyond tracking national averages or interest rate headlines. The forces driving rising home prices in Illinois are deeply rooted in local economic factors: sector-specific job growth, shifting demographics, and unique consumer behaviors all play pivotal roles. To make sense of why Illinois bucks national expectations, you need to look closely at these local dynamics shaping today’s housing reality.

For instance, many homeowners are opting for universal design features in their homes, making them more appealing to a wider range of buyers. This trend is coupled with an increased interest in remodeling, as seen in the budgeting guide for Lake County remodels, which provides insights into the costs associated with such projects.

When it comes to renovations, choosing the right materials is crucial. Homeowners should consider the best materials for their Illinois renovation to ensure durability and aesthetic appeal. Additionally, maintaining a clean and organized space during these renovations can be challenging. For example, keeping your kitchen counter neat and clean is essential for both functionality and visual appeal.

Finally, outdoor spaces are also becoming increasingly important in the housing market. Features like screened houses are gaining popularity in areas like Gurnee, Illinois, providing homeowners with a versatile space that can be enjoyed year-round.

Current State of the Illinois Housing Market

The Chicago real estate market continues to defy conventional expectations, with home price trends in Illinois breaking previous records in mid-2025. According to the latest 2025 housing data, the median sale price for single-family homes across Illinois reached $332,000 in June—marking a 7.4% year-over-year increase. The Chicago metropolitan area leads these gains, where median prices for detached homes now hover at $415,000, up from $385,000 twelve months ago.

Price Growth Across Chicago Neighborhoods

Different neighborhoods are experiencing varied levels of appreciation:

- Logan Square: Median home prices surged by 9% since mid-2024, fueled by ongoing demand from young professionals.

- Hyde Park: Family-sized properties have appreciated nearly 8%, as buyers look for larger living spaces near transit and parks.

- Lincoln Park: Despite already-high prices, the median sale value increased by 6%, driven by limited inventory and strong school districts.

- South Loop: Condo prices rose 7.2%, reflecting renewed interest in downtown living as workplaces adopt hybrid models.

Homeowner Perspectives

“We listed at $490,000 and received six offers within a week—three above asking,” says Rachel M., who recently sold her Edgewater bungalow. “Even with rates nearing 7%, buyers weren’t deterred.”

Illinois homeowners acknowledge higher monthly payments but point to fierce competition as a persistent feature of the market:

- Bidding wars remain common, especially for updated or move-in ready homes.

- Many sellers receive multiple offers despite increased borrowing costs.

- First-time buyers report stretching budgets or seeking co-borrowers to secure a property.

“We lost out on two houses before finally winning a bid in Oak Park,” shares David L., a first-time buyer. “The higher rates hurt, but we couldn’t wait any longer—the market just keeps climbing.”

Buyers and sellers alike are adapting quickly. Strategies include offering flexible closing dates, waiving contingencies, or even writing personal letters to stand out among competing bids.

With price growth outpacing both wage gains and national averages, the Illinois market’s resilience reflects unique local dynamics that continue to shape behavior on both sides of the transaction.

Remodeling Trends in Response to Market Conditions

As the housing market becomes increasingly competitive and prices surge, many homeowners are opting for renovations to enhance their property value. This trend is particularly evident in areas like Lindenhurst, where homeowners are investing in bathroom remodels to attract potential buyers.

Moreover, with families seeking more space due to remote work or hybrid models, there’s a growing interest in expanding living areas. Homeowners are deliberating over whether to add a screened porch or sunroom based on their specific needs and preferences.

In addition to bathroom renovations and outdoor expansions, many are also focusing on maximizing their existing space. For instance, incorporating smart bathroom storage ideas can help manage

Impact of Rising Interest Rates on Housing Affordability

Mortgage rates in 2025 have reached an average of 6.72% for a 30-year fixed loan, a substantial increase from the 3.25%–3.5% range seen just before the pandemic. With borrowing costs nearly doubled, housing affordability in Illinois faces new pressures. Buyers entering the market now face monthly payments that are hundreds of dollars higher than those who locked in lower rates just a few years ago. For example, on a $350,000 home with 20% down, the difference between a 3.5% and 6.72% rate can mean more than $500 extra per month.

Typical Effects of Rising Interest Rates

- Reduced purchasing power: Higher rates usually force buyers to lower their price range or increase down payments.

- Decreased demand: Across most U.S. markets, rising rates slow buyer activity and cool competition.

- Affordability squeeze: First-time buyers and those with moderate incomes get priced out or must compromise on location or size.

Why Illinois Defies the Trend

While these effects are evident nationwide, Illinois stands apart due to persistent demand pressures:

- Strong local employment: Robust job growth in sectors like healthcare and hospitality gives buyers confidence to stretch budgets even as borrowing costs climb.

- Limited inventory: Fewer homes available keeps competition fierce—demand consistently outpaces supply.

- Lifestyle shifts: Ongoing preference for more space or suburban living intensifies demand in key markets around Chicago.

“Even with higher mortgage rates, we had multiple offers above asking,” shares a Naperville homeowner who sold in spring 2025.

The combination of high demand and limited supply creates an environment where borrowing costs impact affordability but don’t dampen price growth as much as elsewhere. This dynamic sets Illinois apart as buyers recalibrate expectations while sellers continue to benefit from strong competition.

In this context, some buyers are exploring alternative housing options such as cedar pergolas or considering renovations through reliable general contractor services to enhance property value amidst rising prices. Additionally, security concerns have become increasingly relevant, prompting some to seek expert advice on home security. Meanwhile, others are opting for kitchen remodeling projects to better suit their evolving lifestyle needs during these challenging times.

Economic Context Influencing the Housing Market

Employment and Labor Market Dynamics in Illinois

Strong employment trends have become a defining feature of the Illinois housing market in mid-2025. Despite national headlines about economic challenges, Illinois employment in 2025 remains resilient. The state’s labor force participation rate has rebounded from pandemic lows, reaching levels that support both homebuyer confidence and sustained demand for residential properties.

Labor Force Participation and Job Growth Impact

Recent data from the Illinois Department of Employment Security highlights a steady rise in labor force participation. As more residents return to work or enter new roles, household income levels remain stable, bolstering purchasing power.

Job growth has not been uniform across all sectors. Healthcare and leisure/hospitality are leading the charge. Hospitals, clinics, and elder care facilities are expanding staff to meet increased demand for services, reflecting broader demographic trends such as an aging population. Similarly, hospitality sees strong recovery as travel and entertainment return to pre-pandemic norms.

Sector-Specific Growth Driving Demand

Healthcare: Hospitals and medical centers in the Chicago metro area continue hiring at an accelerated pace. This sector’s stability provides a reliable base of middle- and upper-income buyers entering or moving within the market.

Leisure/Hospitality: Restaurants, hotels, and event venues have reopened fully with robust bookings. Service workers—often renters—are increasingly seeking entry-level homes or condos, creating persistent pressure on starter home inventory.

“We’re seeing nurses, technicians, and hospitality managers who couldn’t buy two years ago now secure mortgages despite higher rates,” notes a Chicago Realtor specializing in first-time buyers.

Income Stability Offsetting Interest Rate Impact

Wage growth in these expanding sectors helps offset some effects of high mortgage rates. Even as monthly payments climb due to elevated borrowing costs, consistent income streams allow buyers to compete aggressively for limited listings.

Anecdotes from local real estate agents reveal that many clients feel confident making offers above list price because job security in healthcare or hospitality gives them long-term financial stability.

Monetary Policy Impact & Inflation Cooling

The Federal Reserve interest rate 2025 remains at 4.33%, part of a continued effort to keep inflation—which peaked above 9% in 2022—in check. By June 2025, inflation cooled to approximately 2.7%. While these measures typically slow broad consumer spending, sustained job growth allows many Illinois households to withstand upward pressure on housing costs.

Monetary policy impact is less dampening here than elsewhere due to localized economic strengths.

Buyers drawn from robust employment sectors find it easier to absorb higher mortgage rates compared to regions facing layoffs or stagnation.

Economic fundamentals unique to Illinois—especially sector-specific labor strength—explain why Illinois Housing Market Mid-2025: Soaring Prices Despite Rising Interest Rates continues defying national cooling trends. These dynamics set the stage for examining how GDP contraction interacts with ongoing consumer behavior and investment patterns that keep demand alive even as cost pressures mount.

Housing Market Trends and Home Improvement Needs

As the housing market continues to thrive despite economic challenges, there’s an increasing demand for home improvement services. This is particularly evident in areas like design and planning, where homeowners seek expert advice to enhance their living spaces.

Moreover, with more people working from home due to stable employment conditions, the need for effective

Economic Output and Consumer Behavior

Illinois started 2025 with a real GDP contraction of -2.2% in the first quarter, which might indicate economic weakness. However, the Illinois housing market has not reflected this decline. Consumer spending remains strong across much of the state—retail activity, restaurant sales, and discretionary purchases continue to show steady numbers in metro areas like Chicago and its suburbs.

The Federal Reserve interest rate in 2025 stayed around 4.33%, a significant change from the aggressive increases that followed inflation peaking above 9% in 2022. As inflation eased to 2.7% by mid-2025, mortgage rates stabilized at high levels around 6.72%. This stability has helped rebuild some consumer confidence. Buyers and investors see less risk of sudden policy changes, encouraging ongoing participation in home purchases and property investment.

Factors Supporting Consumer Confidence

Several factors are supporting consumer confidence in Illinois:

- Ongoing labor force participation: Many households are protected from broader economic uncertainty due to steady involvement in the labor market.

- Incremental job growth: Gradual increases in employment opportunities provide stability to families and boost their purchasing power.

- Investment trends: Capital is flowing into both residential upgrades and new developments, particularly in neighborhoods experiencing localized employment booms.

- Perception of housing as an investment: Despite softness in GDP figures, strong consumer behavior indicates that residents view housing as a valuable investment—a safeguard against both inflation and future interest rate hikes.

These dynamics reinforce market momentum even when broader economic indicators suggest caution. The interaction between monetary policy impact, job growth, and strong consumer confidence explains why Illinois home prices continue to rise despite challenges in the overall economy.

Factors Driving Persistent Demand Despite Higher Costs

Robust local economic strengths continue to shape the Illinois Housing Market Mid-2025: Soaring Prices Despite Rising Interest Rates. Chicago’s economic resilience has been anchored by sector growth in healthcare and hospitality, helping buffer the market from broader downturns seen elsewhere in the state. Even as manufacturing and government employment retrench, these expanding industries fuel steady job creation and sustain buyer confidence.

Key Local Market Drivers

- Healthcare Expansion: New hospital projects and expanded medical campuses around Chicago and its suburbs have brought a surge of new employees seeking nearby housing. Medical professionals often prioritize proximity, which increases competition for homes in neighborhoods like Oak Park, Hyde Park, and Evanston.

- Hospitality Sector Growth: Downtown Chicago’s hotel and restaurant scene rebounded strongly post-pandemic, adding thousands of jobs. Workers in this sector are driving demand for both rental units and starter homes close to major transit lines.

- Resilient Income Streams: Dual-income households where at least one earner works in these stable sectors report more confidence bidding above asking price, even with higher mortgage payments.

“We moved to Naperville when my wife started at the new hospital; we knew rates were up but found ourselves in a bidding war,” shares Mark, a recent buyer. “It was stressful, but we didn’t want to lose out on the right location.”

Demographic and Lifestyle Influences on Housing Demand

Illinois population trends for 2025 reveal shifts that go beyond simple headcounts. Urban migration towards Chicago suburbs is underway as families seek more space and remote work continues reshaping preferences.

- Population Shifts Within State: Many buyers exiting central Chicago neighborhoods cite affordability pressures or a desire for larger homes. Suburbs like Schaumburg, Arlington Heights, and Bolingbrook have seen notable inflows from city dwellers.

- Remote Work Revolution: Homeowner experiences highlight new priorities—flexible spaces for home offices, larger yards for children or pets, and access to parks or trails. The shift drives up demand for single-family homes just outside the urban core.

- Adapting to Change: Some long-time residents choose to renovate rather than relocate, leveraging home equity built over years of appreciation. Others accept longer commutes or adjust their must-have lists to stay within budget constraints.

Anecdotes from Homeowners:

- A teacher relocating from Logan Square describes losing out on three properties before landing a split-level in Elmhurst—“We had to increase our offer each time because there were always multiple bids.”

- An IT consultant working remotely since 2023 decided to move his family from downtown into the western suburbs: “We needed more space for our kids’ remote schooling setups.”

Sector growth housing demand remains strong due to these interconnected economic and demographic forces. Localized market drivers ensure continued competition among buyers despite higher borrowing costs—a trend echoed across homeowner stories throughout Illinois.

Adapting Homes for New Needs

As families seek more space due to remote work or changing lifestyle preferences, many are considering home expansions. In areas like Lake County, homeowners are faced with the decision of whether to opt for a [second-story addition](https://rohrerforconstruction.com/second-story-addition-vs-main-floor-expansion-options-for-lake-county

Challenges Faced by Homebuyers and Sellers in Mid-2025

Challenges for Homebuyers

Rising mortgage rates have created a steep barrier for buyers across Illinois. With 30-year fixed mortgage rates hovering around 6.72%, the typical monthly payment on a median-priced home in Chicago now exceeds $2,650, excluding taxes and insurance. For many first-time buyers, these higher costs represent a major hurdle—not just in terms of monthly budgeting but also when it comes to qualifying for a loan. Lenders have tightened credit standards, making the process even more daunting.

Key buyer affordability challenges in Illinois:

- Higher down payment requirements: Saving for a down payment has become more difficult as prices continue to climb.

- Debt-to-income ratio constraints: Lenders scrutinize these ratios more closely, especially with larger mortgages.

- Mortgage qualification hurdles: Many buyers find themselves priced out or forced to settle for less desirable neighborhoods due to stricter lending criteria.

Challenges for Home Sellers

On the seller side, low inventory and sustained demand put them in a powerful position. Seller market conditions in Chicago mean bidding wars are common. Listings that are priced competitively often receive multiple offers within days. Sellers can negotiate for minimal contingencies and shorter closing timelines.

“We listed our Logan Square condo on a Thursday and had eight offers by Sunday,” reports one Chicago homeowner. “Every offer came in above asking price.”

Impact of Competition on Buyers

Prospective buyers describe frustration as homes sell before they can schedule viewings. The intense competition encourages some to waive inspections or offer appraisal gap coverage, escalating risks but providing an edge in negotiations.

Influence of Inventory Levels

Low inventory levels amplify these pressures. For every home that hits the market, eager buyers—many relocating from higher-cost coastal cities—drive up prices and keep sellers firmly in control of negotiations.

This dynamic is pushing both buyers and sellers to adapt strategies quickly as they navigate Illinois’ unpredictable mid-2025 housing landscape.

Future Outlook for the Illinois Housing Market

The Illinois housing forecast 2025–2026 depends on several interconnected factors: interest rates, overall economic stability, and how effective policy responses are. Buyers and sellers throughout the state are dealing with a market influenced by these elements, which could lead to very different outcomes based on how each one plays out.

Interest Rate Projections and Market Stabilization Scenarios

Rising mortgage rates—currently hovering around 6.72%—remain a crucial factor. If rates go up further due to ongoing inflation or actions taken by the Federal Reserve, it will become even more difficult for people to afford homes:

- Further rate hikes could sideline more first-time buyers, slow price growth marginally, and lengthen time-on-market for listings in some submarkets.

- Stable or falling rates would likely reinvigorate pent-up demand, unleashing buyers who have been waiting on the sidelines for relief. This could sustain or even accelerate price appreciation in high-demand areas, particularly Chicago’s near suburbs and select urban neighborhoods.

Inflation control efforts play a significant role. Should inflation remain contained near 2–3%, confidence in long-term homeownership typically strengthens, supporting steady transaction volume even at elevated borrowing costs. Conversely, renewed inflation spikes could prompt renewed rate increases and restrict household budgets further.

Policy Recommendations and Market Adaptations

Policymakers and industry leaders face mounting pressure to address rising costs without undermining the underlying strength of Illinois’ housing market. Several strategies offer pathways to increased affordability:

1. Support Affordable Housing Initiatives

- Expand state and municipal investment in affordable housing construction.

- Streamline zoning approvals for multifamily developments near transit corridors.

- Offer targeted down-payment assistance for first-time buyers in high-cost areas.

2. Encourage Lending Adjustments

- Foster innovation among lenders—such as shared equity programs or adjustable-rate mortgages with caps—to help buyers manage monthly payments.

- Incentivize banks to pilot low-down-payment products tailored to moderate-income households.

- Partner with local credit unions to increase access to mortgage credit for underserved communities.

3. Balance Supply Constraints

- Incentivize owners of underutilized properties—vacant lots or aging multifamily units—to bring supply online through tax credits or expedited permitting.

- Support adaptive reuse projects converting commercial buildings into residential units.

Homebuyer education remains crucial as well: workshops on budgeting for higher rates, understanding adjustable-rate options, and navigating competitive bidding can empower consumers facing daunting market conditions.

“If you’re not adapting your approach—whether as a policymaker, lender, or buyer—you’re going to struggle in this new normal,” notes one Chicago real estate agent who’s guided dozens of families through this evolving landscape.

The next year will test Illinois’ resilience—and its ability to innovate—against ongoing affordability pressures. Keeping a close eye on Illinois housing policy, interest rate projections, and lending adjustments offers the best chance of staying ahead in this complex market environment.

Conclusion

The housing market in Illinois is expected to remain competitive with rising prices, even though mortgage rates are still high. Buyers are facing higher monthly payments and affordability challenges, but many are still determined to buy a home. They are adjusting their strategies by looking for homes in different locations or being flexible with property features.

Sellers in Illinois are benefiting from low inventory, which gives them an advantage in negotiations. This means they can sell their homes for higher prices or have more control over the terms of the sale.

The job sectors that are doing well in Illinois, such as healthcare and hospitality, are helping to balance out any economic downturns. This is good news for the housing market because it means there will still be demand for homes even if the overall economy is struggling.

Both buyers and sellers need to be adaptable in this challenging market. By staying informed about new lending options and market trends, they can find opportunities to make successful transactions.

The future of the housing market in Illinois will depend on how everyone involved responds to changing conditions. It’s important for buyers, sellers, real estate agents, and policymakers to work together towards sustainable growth and affordability in order to create a better housing market for all.

FAQs (Frequently Asked Questions)

Why are home prices in Illinois soaring despite rising mortgage interest rates in mid-2025?

Home prices in Illinois, particularly in the Chicago metropolitan area, continue to rise despite higher mortgage rates (~6.72% for a 30-year fixed) due to persistent demand pressures fueled by robust local economic factors such as employment growth in healthcare and hospitality sectors, population shifts favoring suburban living, and ongoing consumer spending that sustains market momentum.

How have rising interest rates affected housing affordability for buyers in Illinois in 2025?

Rising mortgage interest rates have increased monthly payments and borrowing costs, creating affordability challenges for many buyers. However, the impact on housing demand is less pronounced in Illinois because strong employment trends and sector-specific income growth help support buyer purchasing power amid competitive bidding environments and low housing inventory.

What economic factors are influencing the Illinois housing market’s resilience amid national economic headwinds?

Illinois’ housing market resilience is supported by stable labor force participation and job growth in key sectors like healthcare and leisure/hospitality, which sustain income levels. Additionally, despite a -2.2% real GDP contraction in Q1 2025, continued consumer spending and investment contribute to maintaining housing demand and price growth locally.

How do demographic trends and lifestyle changes impact housing demand in Illinois during mid-2025?

Population shifts within Illinois, including urban migration toward Chicago suburbs and preferences for larger homes influenced by remote work trends, are driving localized demand increases. These demographic and lifestyle factors contribute to sustained buyer interest and competitive market conditions despite higher costs associated with rising interest rates.

What challenges are homebuyers and sellers facing in the Illinois housing market as of mid-2025?

Homebuyers face increased monthly mortgage payments due to elevated interest rates, making affordability a significant hurdle. Sellers benefit from low inventory levels and strong demand, giving them advantages during price negotiations. Buyers often encounter competitive bidding scenarios and stricter mortgage qualification requirements amid these dynamics.

What is the future outlook for the Illinois housing market through 2026 considering current economic conditions?

The Illinois housing market may experience stabilization or continued price growth depending on interest rate movements—whether they rise further or hold steady around current levels (~4.33% Federal Reserve rate). Ongoing inflation control efforts, affordable housing initiatives, lending innovations, and policy adaptations will play crucial roles in addressing affordability concerns while supporting market strength into 2026.

news via inbox

Nulla turp dis cursus. Integer liberos euismod pretium faucibua